![]()

Executive Summary

- There are good reasons for Malaysia to follow the example of the 70 national and subnational jurisdictions which already utilise carbon pricing as a critical tool in climate policy making

- A carbon tax applied to the electricity, transport, and oil and gas sectors will cover over 70% of annual national emissions, and help ensure that Malaysia meets, or even exceeds, its climate goals

- A carbon-pricing scheme commencing at a rate of RM35/tCO2e in 2020 and gradually rising to RM150/tCO2e by 2028 would raise an annual average of RM21.8–24.6bil in federal revenues over the next decade.

- “Carbon rebates” need to be prioritised to lessen the regressive burden posed by carbon pricing on B40 households. It is recommended that 29-45% of aggregate revenues be redistributed in the form of such rebates, which can be dispersed through the existing Bantuan Sara Hidup grant framework

- Carbon revenues should also be utilised to further climate change mitigation and adaptation efforts, for which there is currently a funding gap of RM20bil, a figure that will rise over time as urgency grows over the need to engage in sustained and strengthened decarbonisation

- As revenues rise over time, carbon pricing can play an indirect role in mitigating inequality by

financing progressive tax system reforms - This policy of carbon price-and-rebate (CPR) can put Malaysia on the path towards long-term sustainability, with few consequential costs in the near future and huge benefits in the medium to long term

Setting the Stage for Carbon Pricing

The Intergovernmental Panel on Climate Change (IPCC) announced in 2018 that unprecedented reductions in emissions are necessary within the next decade to prevent an average global surface temperature rise of more than 1.5°C over preindustrial times. Such an increase would exacerbate sea-level rise; render more common extreme weather events such as storms, floods, droughts, hurricanes and tsunamis; adversely affect health and mortality; and threaten ecosystems and biodiversity, as well as agricultural yields.

One policy mechanism that has the potential to play an important role in addressing these issues is the enforcement of a tax on greenhouse gas (GHG) emissions. Such a policy would directly and significantly boost public finances, enhance the competitiveness of low-carbon technology, spur the growth of local green industry, and contribute to Malaysia meeting its international climate goals. Finally, the redistribution of carbon revenues can directly offset any immediate regressive effects of the tax and indirectly assist in the achievement of other economic policy goals, including those pertaining to climate change.

The Economics of Carbon Pricing

Climate change is being caused largely by the rapid increase in the atmospheric concentration of carbon since the Industrial Revolution, and is the result of two market failures: negative externalities in the form of emissions and a global public good in the form of the atmosphere.

In countries like Malaysia where markets do not recognise the social costs of carbon emissions that are the negative externalities of otherwise productive economic activity, these emissions are oversupplied. Meanwhile, when “access” to a public good such as the atmosphere, characterised by the qualities of non-rivalry and non-excludability[1], is unpriced, it is overused. Consequently, increases in both emissions and the atmospheric carbon concentration are entirely unsurprising.

Corrective policymaking through the creation of a market for emissions and subsequent “use” of the atmosphere is therefore possible and necessary, and is most efficiently done through the pricing of carbon. With emissions priced in a manner that reflects their societal cost, emitters and consumers alike are forced to re-optimise profit- and utility-maximising behaviour by embedding these costs into their private decision-making.

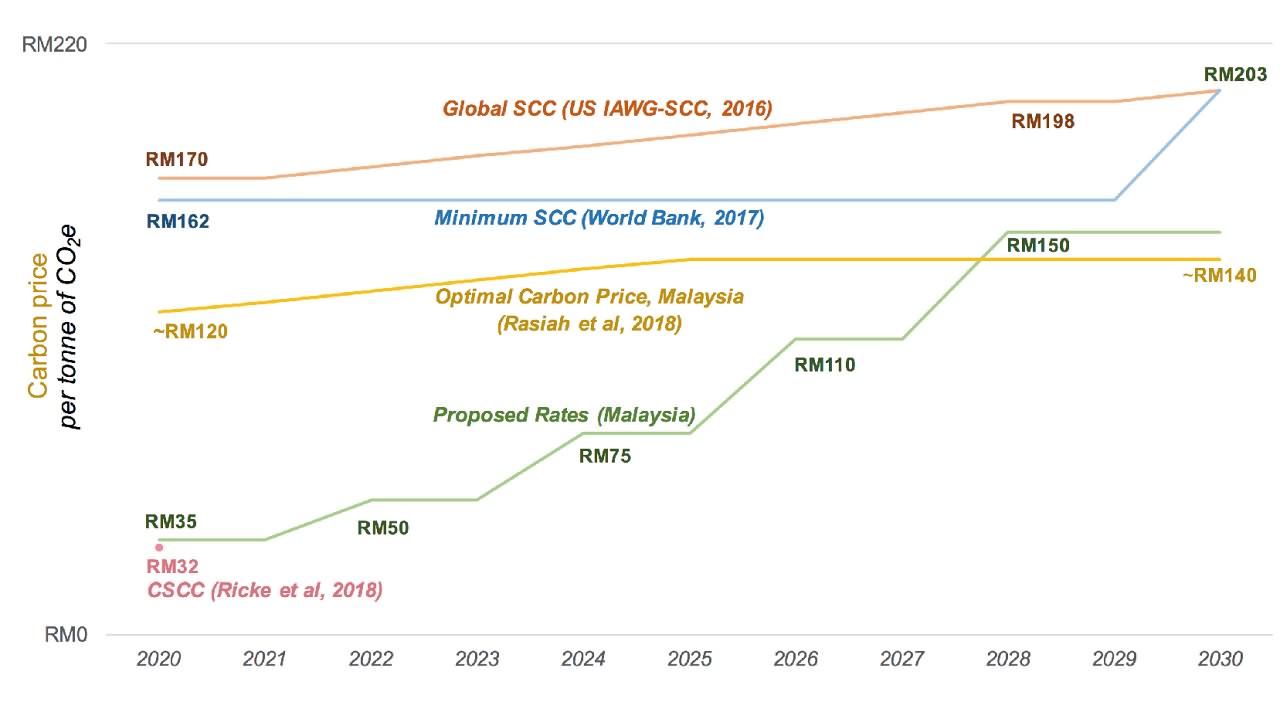

The social cost of carbon (SCC) is today widely used to measure the economic value of the damage caused by each incremental ton of CO<sub2e emitted into the atmosphere. In 2010, the US government developed what is broadly considered to be one of the most comprehensive estimates of the (global) SCC, currently of around US$42/tCO2e (or RM170/tCO2e) and rising to $50 (RM203) in 2030. Meanwhile, World Bank (2017) cites a present-day figure of $40–80/tCO2e as being necessary for emissions reduction outcomes to be consistent with the temperature goals set within the Paris Agreement.

As of 2018, a total of 45 national and 25 subnational carbon pricing schemes have been either implemented or scheduled for implementation across the world, covering around a fifth of total global emissions (World Bank, 2018). The SCCs utilised across these schemes vary tremendously: being as low as under US$1/tCO2e in Mexico, Poland, and Ukraine, and as high as US$139/tCO2e in Sweden.

Crucially, however, most prices used across these schemes are considerably lower than both the US government and World Bank estimates, with only France, Finland, Liechtenstein, Sweden, and Switzerland presently meeting them. The selection of an excessively-low SCC is unlikely to stimulate lasting and sufficient decarbonisation because of its inadequacy in addressing the externality costs of emissions. In solving the externality problem, carbon must be priced at rates reflective of scientific and economic evidence; and in solving the public good issue, some uniformity in the price used across jurisdictions is needed.

In order to minimise the short-term economic and political costs associated with the immediate adoption of a steep carbon price, early-adopters tend to implement schemes where the SCC rises gradually over time. These include, but are not limited to, existing and planned carbon taxation frameworks in the Canadian states of Alberta and British Columbia; in France; the Netherlands; and Singapore[2]. It is herewith proposed that Malaysia embraces this gradualist approach.

A Proposal for CPR in Malaysia

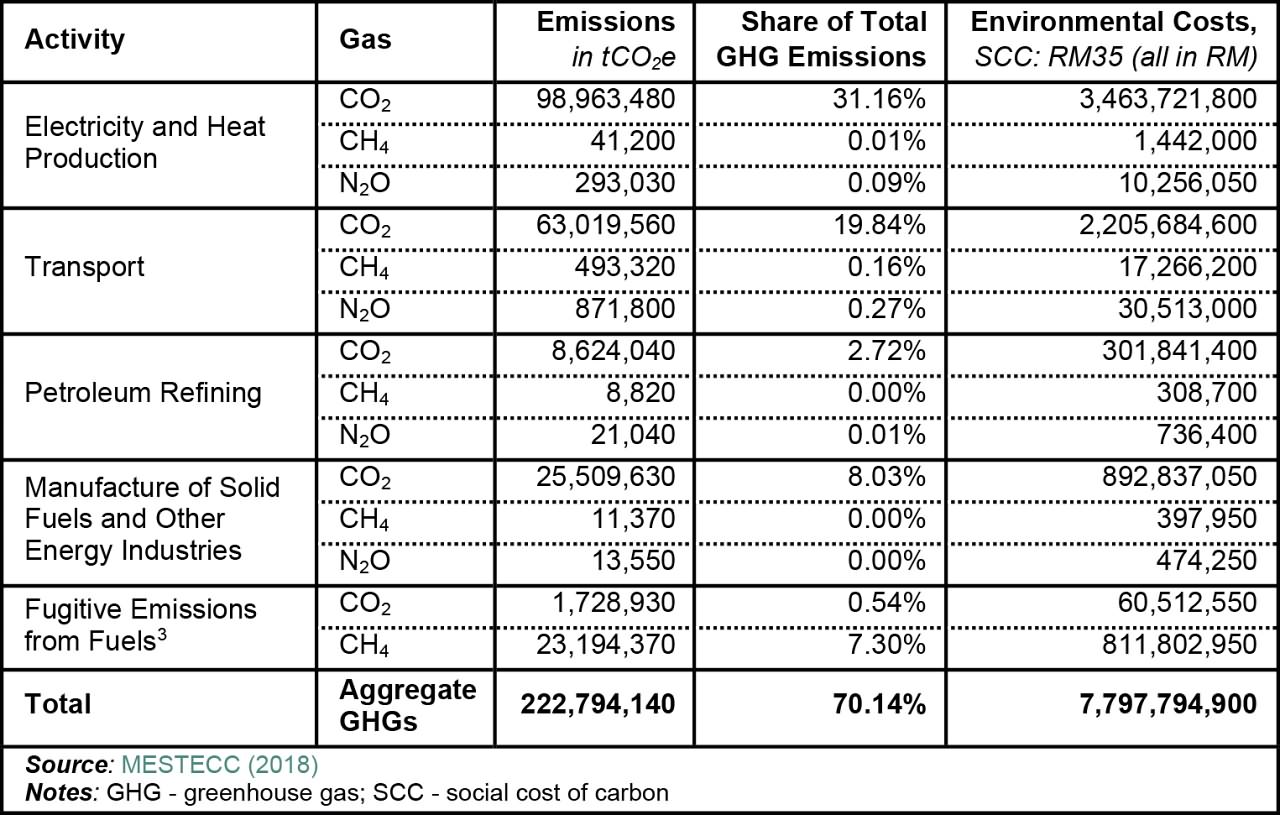

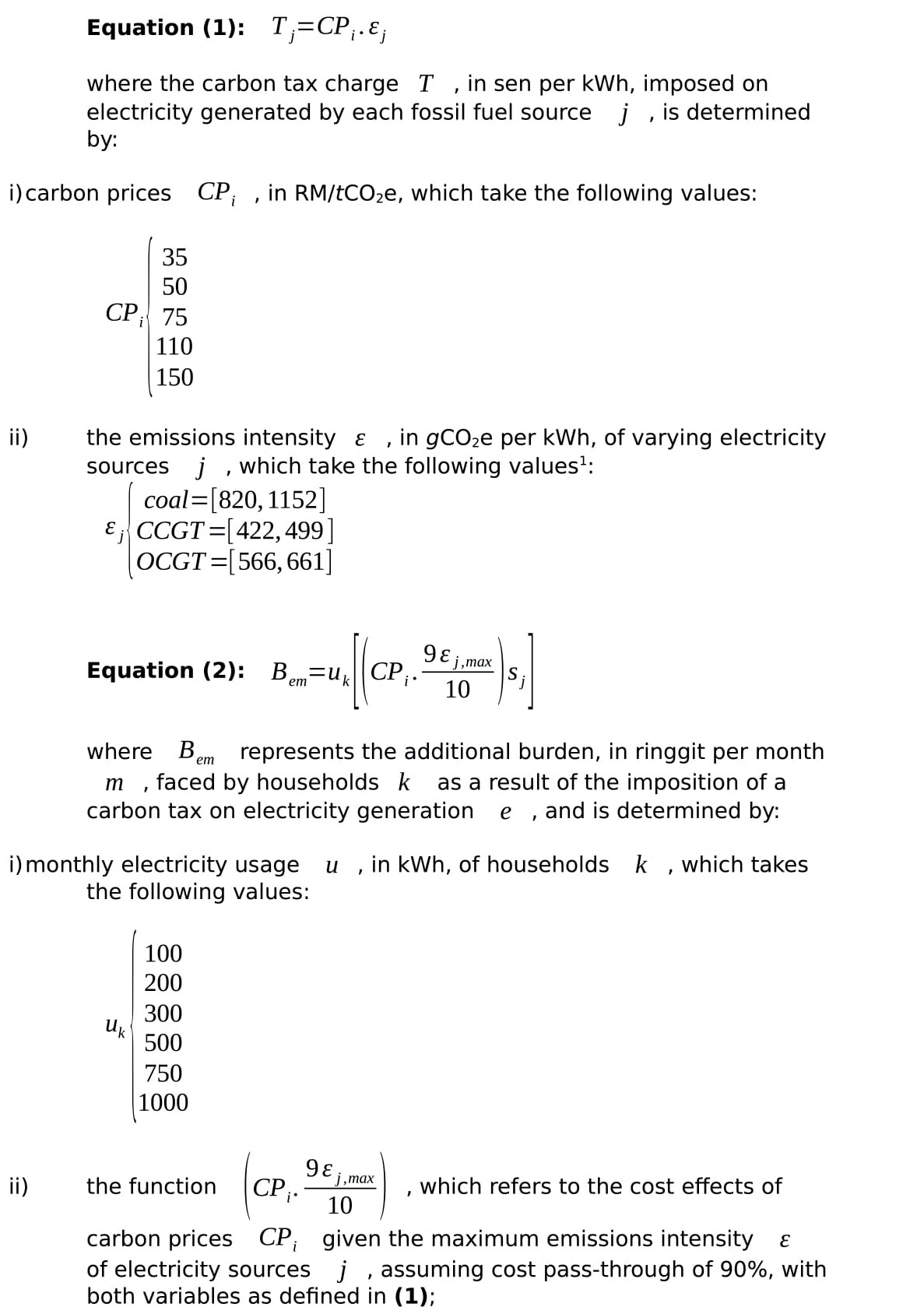

This paper proposes a downstream carbon pricing framework for Malaysia with an initial coverage of three heavily emitting economic sectors—in electricity, transport, and oil and gas production; and incorporates a cost of carbon which rises gradually from RM35/tCO2e in 2020, to RM150/tCO2e between 2028 and 2030. An overview of the scope and rates of this policy proposal are provided in Table 1 and Figure 1 respectively.

Table 1: Major Sources of GHG Emissions in Malaysia, 2014

Pricing emissions at their source[4] has the advantage of allowing polluters within the relevant sectors to select from a wider range of emissions abatement options than would generally be the case under an upstream carbon policy that imposes taxes predominantly on fossil fuels at their point of extraction.

Given that in Malaysia, carbon-intensive electricity is largely generated by no more than a handful but separate entities; oil and gas production emissions are almost entirely the responsibility of a single multinational; and transport fuel prices are regulated on a national level; transaction costs associated with such downstream regulation are minimised.

Firms subjected to carbon pricing seek to minimise costs by reducing pollution levels to the point where marginal costs of adopting abatement measures are equivalent to the cost of carbon. As the carbon price increases over time, a greater number of abatement options fall into this category, adding further momentum to the process of emissions reduction.

Under this proposal, carbon prices are to be revised every two years after commencing at a rate of RM35/tCO2e in 2020. This figure is reflective of Malaysia’s “country-level” social cost of carbon (Ricke et al, 2018) and falls within the lower end of the range of carbon prices implemented in numerous other nations at present; it is, for instance, roughly equivalent to the SCCs used to inform Portugal’s carbon tax and Beijing’s emissions trading scheme.

The predetermined biennial revision of rates mitigates policy uncertainty and allows economic actors the ability to project and make longer-run business decisions in the presence of a transparent and predictable carbon pricing scheme. By the end of the decade, it is recommended that the emissions price rises to RM150/tCO2e; much closer to the SCC estimates of both the US government and the World Bank. This ultimately puts Malaysia in a strong position to adapt to an eventual global pricing regime at rates consistent with scientific evidence. Such a framework would ensure a proper addressing of market failures contributing to climate change.

Estimating the Sectoral Effects of Carbon Pricing

The implementation of a price on carbon will have a significant impact on the Malaysian economy. Recognising emissions as a tangible economic cost will have direct repercussions for emissions-intensive industry players and provide benefits to low-carbon industries. Such price effects are theorised to propel changes in the production and consumption behaviour of economic actors by incentivising the adoption of sustainable practices and technologies. Investigating the impact of carbon pricing on the electricity, transport, and oil and gas industries, as well as consumers, is the aim of this section.

On Electricity Generation

The role the electricity industry can play in climate change mitigation cannot be understated. First, it is the single-largest contributor to national emissions, accounting for about a third of the total. Second, renewable energy (RE) technologies are increasingly able to replace fossil fuels as the predominant sources of energy, from both technical and economic standpoints. On the demand side, the application of energy efficiency measures, the use of smart technology, as well as the liberalisation of electricity markets lend themselves to the possibility of further reductions in emissions. The pricing of carbon hastens electricity sector disruption by enhancing the economic competitiveness of low-carbon technologies by placing a tangible value on the environmental costs associated with the use of fossil fuels.

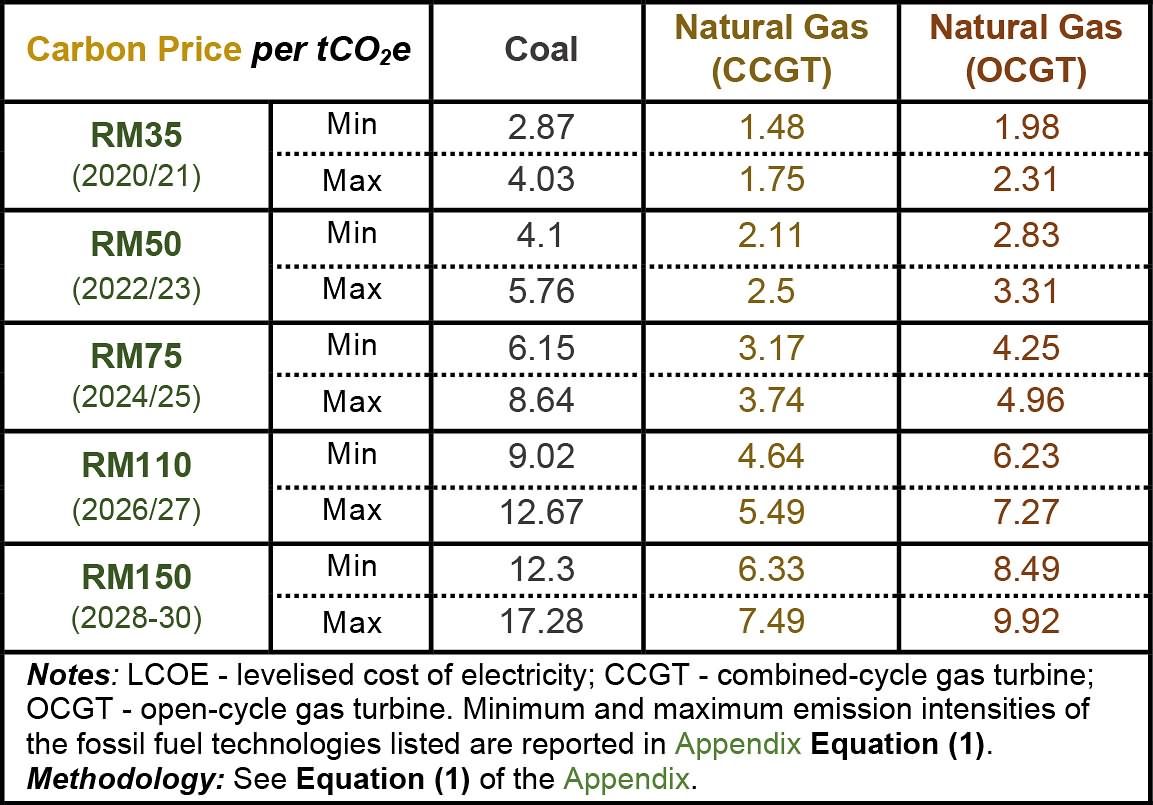

This idea is summarised in Table 2, which details the impact of carbon pricing on the levelised costs of electricity (LCOE) for coal and natural gas[5]. Ultra-supercritical coal power plants, which emit approximately 820gCO2e per kWh of electricity produced, would be subjected to a levy of roughly 2.87 sen/kWh at a carbon price of RM35/tCO2e; for older, less efficient coal plants, the figure is closer to 4.03 sen/kWh. The levies on natural gas power production are smaller, owing to the fact that it is roughly half as polluting as coal, with slight disparities between combined-cycle gas turbines (CCGT) and less efficient open-cycle alternatives (OCGT). These marginal effects grow with any increases in the underlying carbon price.

Table 2: Carbon Taxes Imposed on Electricity Generated by Coal and Natural Gas Power Plants in sen per kWh

To put these marginal price effects into perspective, Table 3 models the LCOE of two ultra-supercritical coal plants (Manjung 5 and Jimah East) and two combined-cycle natural gas plants (Seberang Perai and Pasir Gudang) in Malaysia at varying carbon rates. Without a price on carbon, the average LCOE for these CCGT plants, at 35.85 sen/kWh, is over 50% higher than that of coal (23.78 sen/kWh).

Carbon pricing minimises this differential; at a rate of RM35/tCO2e, the differential falls to around 39%, and at RM150/tCO2e, to only 14.2%. Tables 2 and 3 confirm that, ceteris paribus, carbon pricing enhances the importance of the emissions intensity of energy sources by eliminating the cost advantages held by cheap, carbon-intensive fossil fuels.

Table 3: Estimated LCOE of Selected Power Plants in Malaysia in sen per kWh

The picture looks brighter still for RE. Figure 2 contrasts the costs of Manjung 5, among the most advanced and efficient coal power plants in South-east Asia, with those of large-scale solar (LSS) plants under varying carbon rates, and at two distinct price points for coal[6]. The horizontal lines reflect averages of the five lowest-cost bids in each LSS auction. For LSS 3 and 4, these are estimates which account for the rate of cost reductions between LSS 1 and 2, as well as projections of LSS capital expenditure costs through 2030[7]. The pricing of carbon greatly enhances the economic competitiveness of solar, and at a carbon price of RM35/tCO2e in 2020 and 2021, LSS 4 is projected to invite bids whose levelised costs, as low as 27.41 sen/kWh, closely resemble those of Manjung 5. A realisation of the long-theorised erosion of the cost benefits of coal-fired electricity through technological development is nearing, and this process is hastened by the pricing of emissions.

Cheaper access to financing can also enhance a firm’s ability to charge lower levelised tariffs. Evidence[8] indicates that first, improved access to loans strictly increases rates of private investment in RE projects, which are typically capital-intensive; and second, variations in the weighted average cost of capital (WACC) across countries is a significant driver of differences in the LCOE of solar technologies across countries[9]. Finally, low interest rate environments are found to make the adoption of green technology more attractive, and the levelised costs of RE technologies are more reactive to interest rate changes than are traditional fossil fuel technologies.

Figure 2: LCOE Comparisons, TNB Manjung 5 and Large-Scale Solar at Varying Carbon Rates

This evidence accentuates the importance of a comprehensive national green financing framework that allows prospective private sector actors favourable and stable access to funding for RE projects. Combined with Malaysia’s natural endowment of solar irradiation and the fact that it is among the leading global producers of photovoltaic panels, there is tremendous potential for the nation to become one of the cheapest countries in generating solar-powered electricity should supportive measures be put in place.

On Electricity Prices

A crucial point of concern within the electricity sector pertains to the effects of carbon pricing on consumer prices, particularly those faced by the B40. In determining the effects of carbon pricing on consumer electricity prices, a liberal estimate of 90%[10] in pass-through costs is assumed to illustrate the worst-case effects of the policy. In Malaysia, electricity tariffs vary across customer category and total monthly consumption, and so the magnitude of the effects of carbon pricing on the end-consumer will vary both across and within sectors.

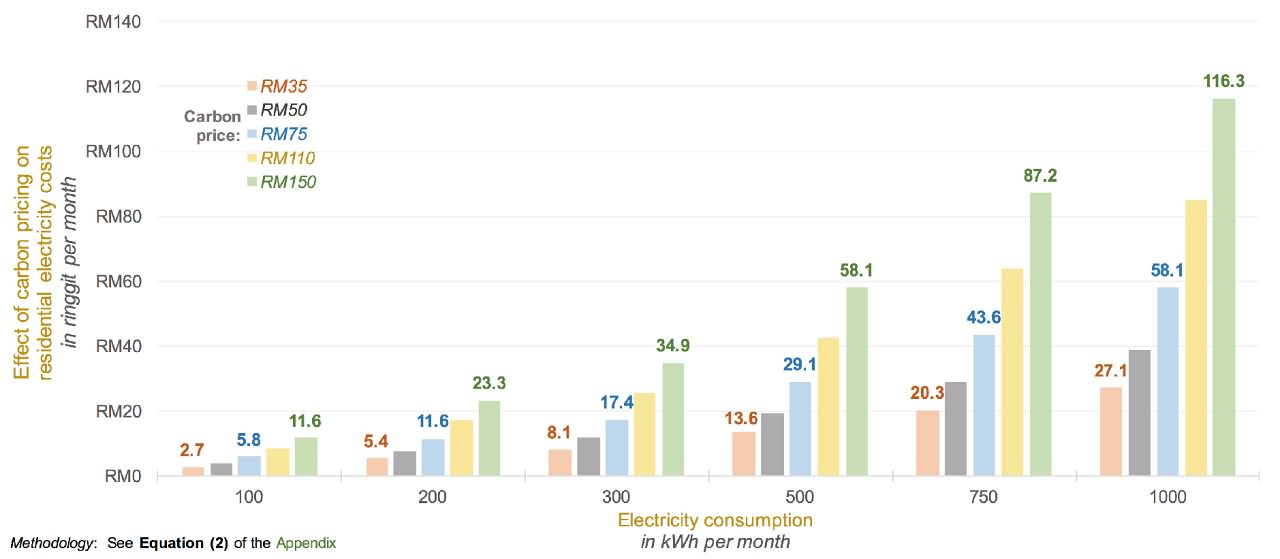

In this report, specific emphasis is placed upon households. Figure 3 projects the effects of carbon pricing on illustrative households across a wide spectrum of electricity usage rates. Given a presumed correlation between income level and electricity consumption, this exercise allows for far-ranging estimations of the distributional effects of carbon pricing.

Figure 3: Worst-Case Effects of Carbon Pricing on Residential Electricity Costs

Two further assumptions are made in estimating these effects: first, the maximum marginal cost impacts of carbon pricing on the LCOE of coal, CCGT, and OCGT, as per Table 2, are used; and second, the assumed electricity generation mix is comprised of 56.5% coal, 34.6% CCGT, and 5.7% OCGT[11], with the remainder either supplied by technologies unaffected by carbon pricing or those whose contributions to total electricity generation are relatively insignificant. Taken together, the three assumptions ensure that the effects detailed in Figure 3 represent the worst-case scenario for marginal electricity price increases as a result of carbon pricing.

At a price of RM35/tCO2e, additional monthly costs range from RM5.40 for households who consume an average of 200kWh of electricity per month to RM27.10 for those consuming

1000kWh. These figures rise to a maximum of RM23.30 and RM116.30 at RM150/tCO2e. For a two-person household in the B40 that consumes around 280kWh of electricity per month[12], the estimated additional burden is less than RM8.10 (at the introductory carbon price of RM35 per ton), rising to a maximum of RM31 per month (at a carbon rate of RM150/tCO2e in 2028). These increases can be managed entirely through the introduction of carbon rebates for the B40, which is a topic discussed later in this paper.

A final note on electricity is that the effects of carbon taxation on electricity prices are dampened as the use of low-carbon energy rises. Should the national RE target of 20% by 2025 be achieved, marginal effects of carbon pricing on electricity prices are estimated to be approximately 31% smaller than at present[13]. Consequently, as the share of RE in electricity generation increases during the course of this carbon pricing regime, its marginal effects on electricity prices will over time be progressively smaller than estimated in Figure 3.

On Transport

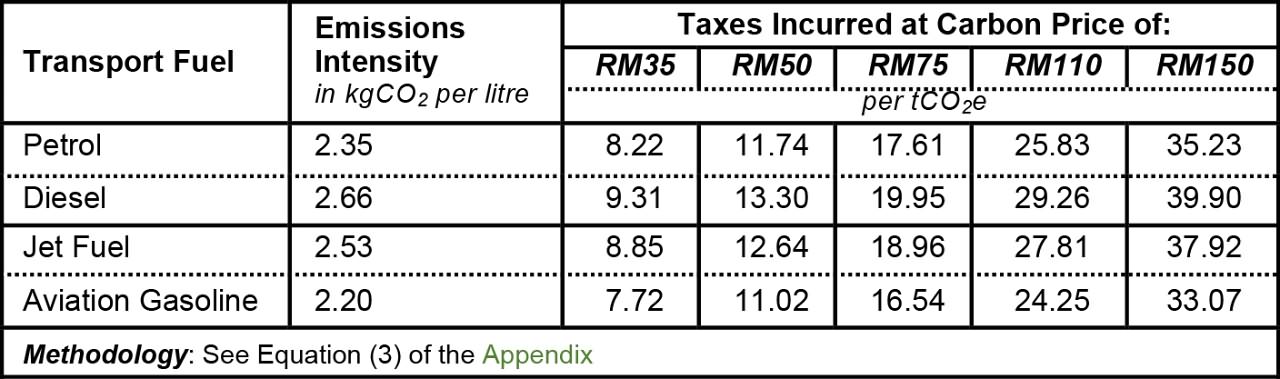

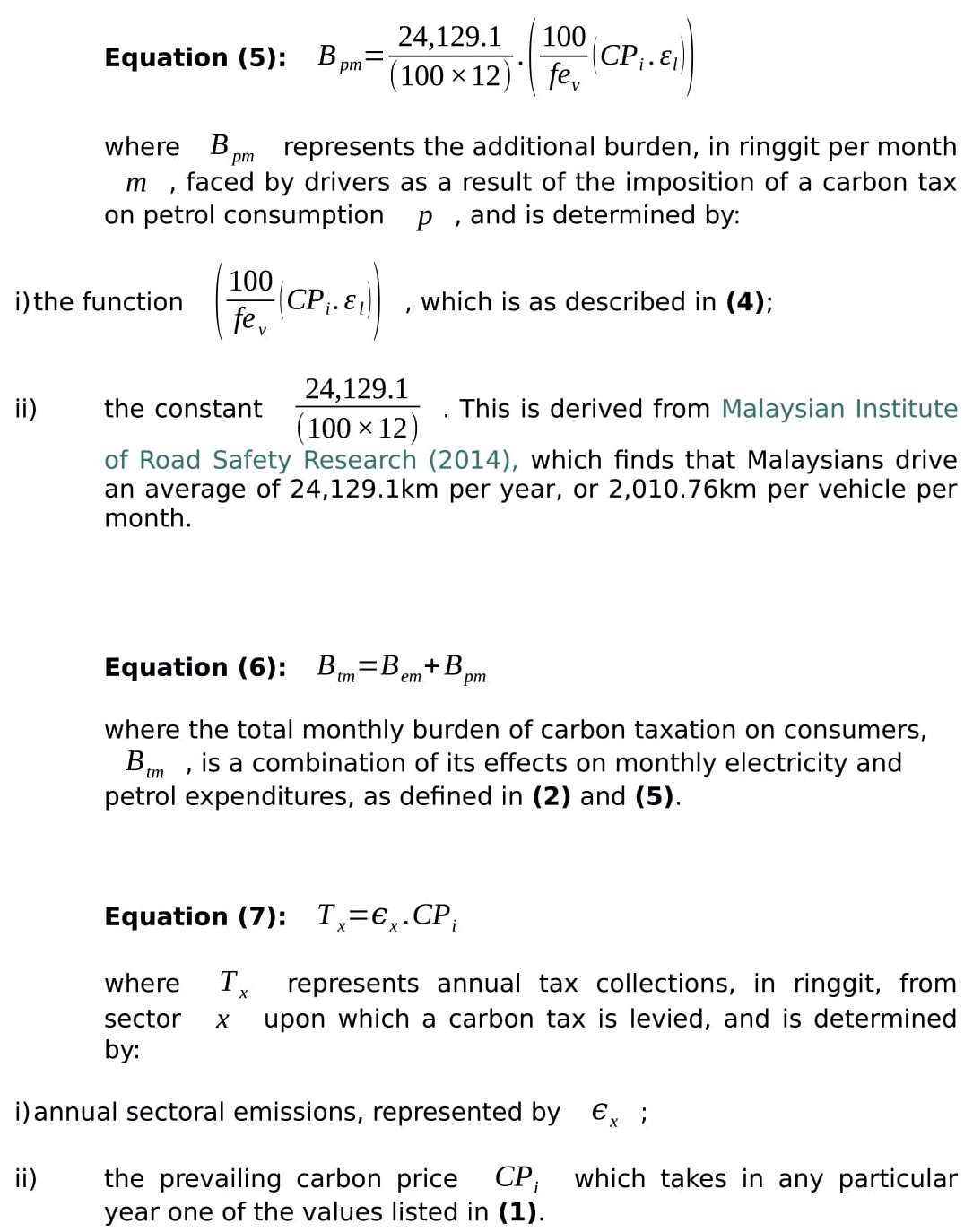

In Malaysia, prices of petrol and diesel are both heavily subsidised and regulated by the government. This latter fact directly limits the transaction costs associated with downstream implementation of carbon pricing within the sector. As a result, it proposed that carbon levies be imposed at the point of refuel. Given that combustion emissions vary across transport fuels, tax rates would also vary across fuel type. A summary of emissions intensities and the marginal effects of carbon pricing on the costs of common transport fuels is provided in Table 4.

Table 4: Carbon Taxes Imposed on Transport Fuels in sen per litre

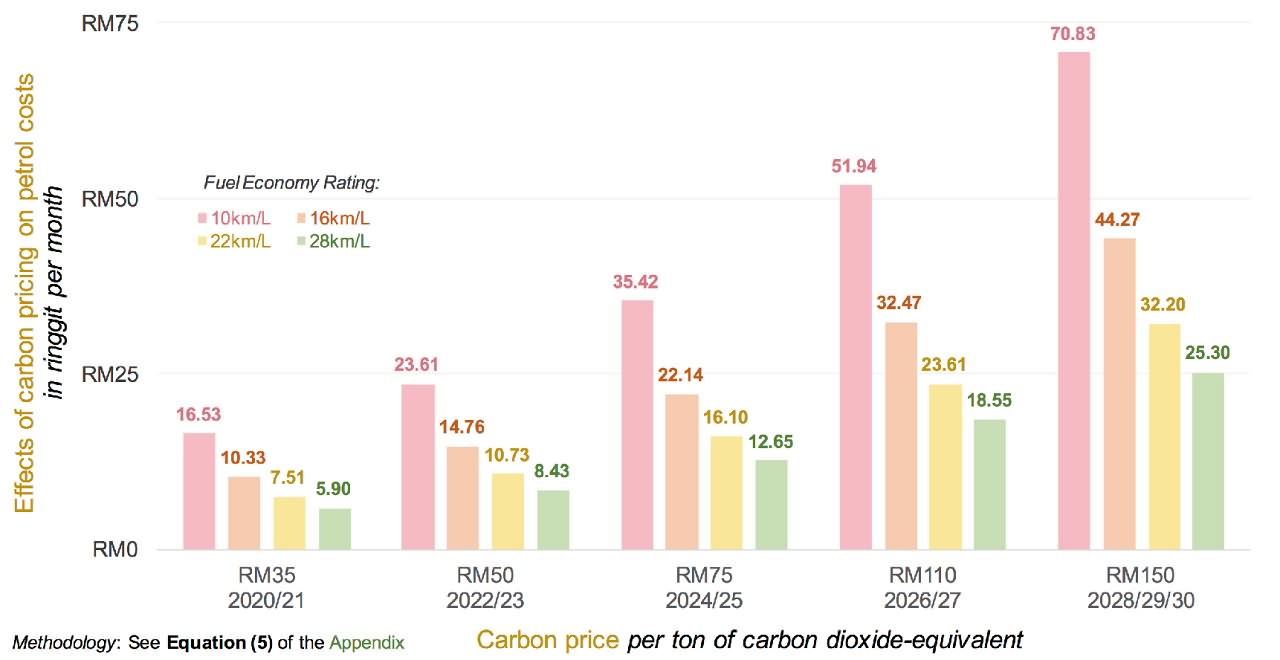

Figure 4 puts into context the relative magnitude of these per litre increases in the prices of petrol[14] across gasoline-powered cars of varying fuel economy ratings. The results have two important features. First, carbon pricing significantly raises the importance of vehicular fuel economy. Cars which achieve 10km per litre of petrol would be faced with additional annual costs over vehicles with an average of 22km/L, of RM106.40 at a carbon price of RM35/tCO2e. This figure rises to RM228.02 at RM75/tCO2e, and RM456.04 at RM150/tCO2e. The influence of fuel economy is so stark that typical hybrid vehicles would face only slightly higher carbon costs at a price of RM150/tCO2e than an inefficient petrol vehicle would at RM50/tCO2e.

Carbon pricing provides a consistent fiscal incentive for cost-conscious consumers to divert more attention to fuel efficiency in future vehicular purchase decisions. In improving average fleet-wide fuel economy, it assists in mitigating the contribution of road transport – the most prominent component of sectoral emissions[15] – to total national emissions. For consumers, benefits extend to reductions in local air and noise pollution, particularly through the use of hybrid and electric vehicles (EVs).

Figure 4: Effects of Carbon Pricing on Average Monthly Petrol Expenditures

Second, the harmful effects of carbon pricing on transport fuel prices are, as with electricity, relatively muted and can be addressed through the provision of carbon rebates. At a modest tax of RM35/tCO2e, most drivers would face additional monthly costs no larger than RM16.53; given that an average fleet-wide fuel economy is closer to 16km/L, additional costs would more likely average approximately RM10 per month. This figure rises to around RM15/month at a carbon price of RM50 in 2022/23, and RM22 at RM75/tCO2e in 2024/25. During this period of rising carbon prices, however, vehicular fuel efficiency is also likely to show improvement. It is plausible that by the time the carbon price rises to RM110/tCO2e in

2025, the average fuel economy of in-use vehicles would be closer to 22km/L, which in turn translates into additional monthly costs of under RM25.

On Public Transportation

The carbon pricing-induced rise in the costs of driving across vehicles and fuel types will have the important complementary effect of encouraging the use of public transportation. This is a second avenue through which the pricing of carbon can lead to major emissions reductions within the sector[16]. Carbon pricing essentially acts as a permanent upward shock in the cost of polluting transport fuels, and studies indicate that increases in the price of petrol are associated with higher rates of public transit ridership. In particular, there is strong evidence that higher petrol prices lead to increased switching from private to public transport among lower-income groups[17]. There is therefore a need to ensure that public transportation networks in Malaysia are prepared to cope with additional demand, as the effects of carbon pricing on fuel costs are felt over time.

Within the Klang Valley, emphasis must be placed on enhancements to first- and last-mile connectivity, as well as measures to alleviate capacity issues on popular transit routes during peak periods. Options include building extensive networks of clearly-defined pedestrian bridges and walkways, ameliorating bus networks and services, and implementing measures to encourage the use of bikes. Traffic congestion is another pertinent problem, and while the pricing of carbon should help in its mitigation, the removal of the long-existing fuel subsidy would likely have more profound direct effects. As average fuel economies rise, public transportation networks improve, and the vehicle fleet electrifies, the political argument for keeping the subsidy will diminish. The Ministry of Finance and the Ministry of Transportation should set a fixed timeline for this to happen.

Beyond KL, investments should be made in improving bus networks and services across all heavily-populated areas of Malaysia, while the development of light-rail or tram services within larger or denser cities such as George Town, Johor Bahru, and Melaka is strongly encouraged. In order to generate momentum for a significant downward push in emissions within the transport sector, taking steps to reduce the number of cars on the road is a necessity[18].

On Oil and Gas

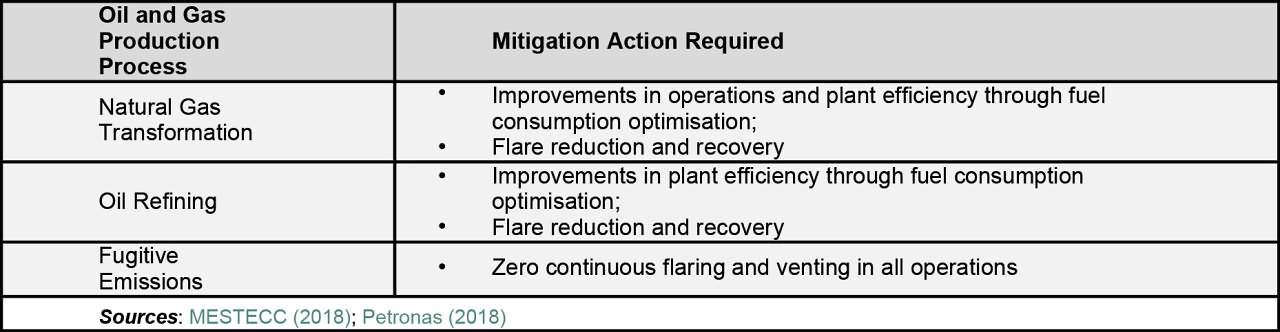

Emissions from oil and gas production processes fall into three major categories: i) emissions from the manufacture of oil, and natural gas transformation; ii) emissions at petroleum refineries; and iii) fugitive emissions, particularly from venting and flaring of gas in oil production, as well as production, processing, flaring, transmission, storage, and distribution emissions associated with natural gas production.

The imposition of a carbon tax within the oil and gas production amounts to a tax that covers most operations of the state oil-and-gas conglomerate Petroliam Nasional Berhad (Petronas). This situation is complicated by the fact that Petronas has long provided the government with special dividends, with the most recent figure amounting to RM30bil (Ministry of Finance, 2018). As far as possible, additional levies imposed on the firm through the pricing of emissions should be treated as distinct to these dividends, which exist for and serve altogether different purposes.

A carbon tax acts as a strong fiscal incentive for all industry players to engage in mitigation action within all three major sectoral emissions categories. Table 5 lists the actions cited by Petronas as necessary to achieve an emissions trajectory in line with the Ministry of Energy, Science, Technology, Environment and Climate Change’s (MESTECC) most ambitious emissions scenario. These should not be seen as an exhaustive list of emissions mitigation options within oil and gas operations; over time, further investment must be made in carbon capture-and-sequestration (CCS) technologies and other carbon-sink strategies, while Petronas should take steps to close some of its more polluting assets.

At the same time, it must be encouraged to invest more in its domestic RE generation capacity, and add to its existing 10MW facility in Gebeng, Pahang. While it has applied an internal carbon pricing mechanism in its assessment of investments and operational design (Petronas, 2018), the enforcement of a tangible national-level tax on carbon is needed to drive the adoption of emissions mitigation action and contribute to immediate emissions reductions within the industry.

Table 5: Emissions Mitigation Options in Oil and Gas Production Processes

Aggregating Carbon Revenues

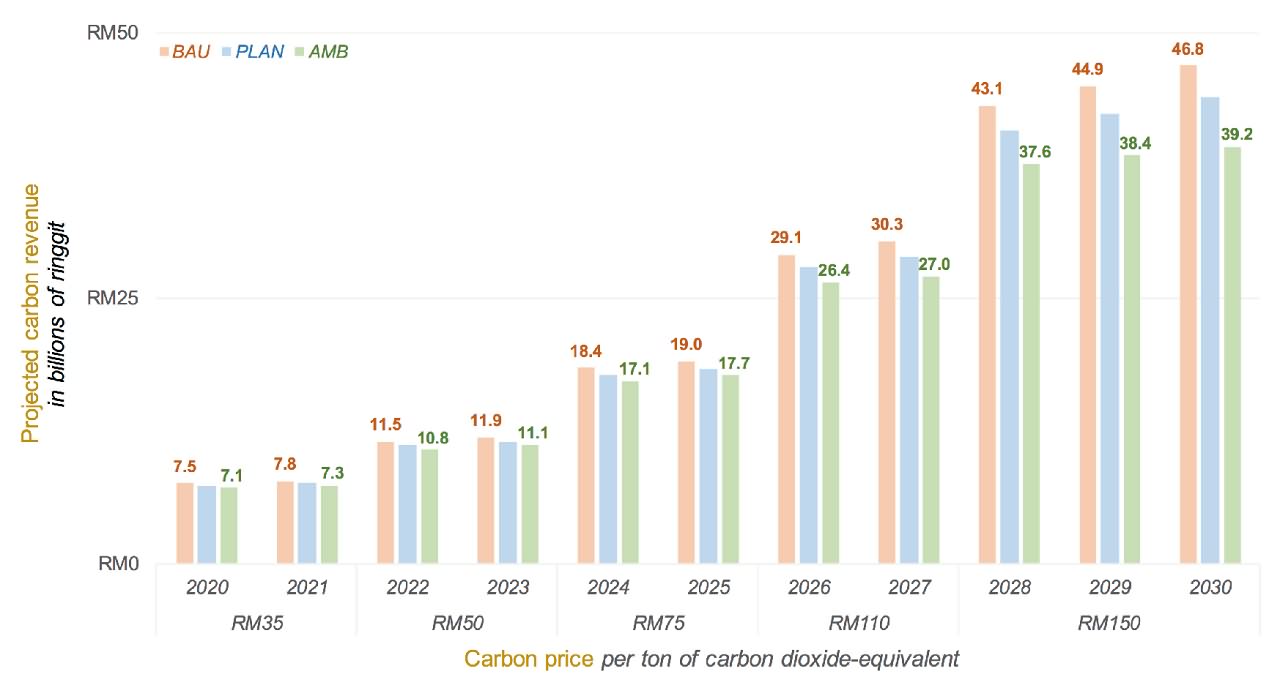

The redistribution of revenue generated by a carbon pricing mechanism is an integral component of addressing its regressive direct effects and maximising its indirect benefits, including providing funding for further climate change mitigation and adaptation measures. With a significant carbon revenue stream, policymakers would over time be in a stronger position to address other economic issues and market failures not necessarily relevant to climate change. Figure 5 depicts total annual revenues from this proposed policy between 2020 and 2030. With just three sectors covered (electricity, transportation, and oil and gas), carbon taxation would yield a substantial magnitude of RM7.5bil in revenue in 2020 at a carbon price of RM35/tCO2e, rising to RM46.8bil in 2030 at a price of RM150/tCO2e.

Figure 5: Aggregate Carbon Revenue Projections, 2020 to 2030[19],[20]

There are four avenues through which these carbon tax revenues are recommended to be utilised. The first two should be prioritised in the short-run, and the latter two during the policy’s existence when carbon prices are higher. First, the regressive direct effects of a tax on emissions should be addressed through carbon rebates to the B40. Second, funding is still required to enable further climate change mitigation and adaptation efforts, as well as to improve national GHG inventory management systems. Third, carbon taxation should in the longer-run form a crucial component of broader, progressive tax reform, with revenues used to fund a progressive overhaul of personal income taxes, reductions in corporate taxation rates, the longer-run abolishment of the Sales and Services Tax (SST), among other measures. Finally, any residual revenues can be utilised to address Malaysia’s existing fiscal issues.

Resuscitating the Economy through Carbon Rebates

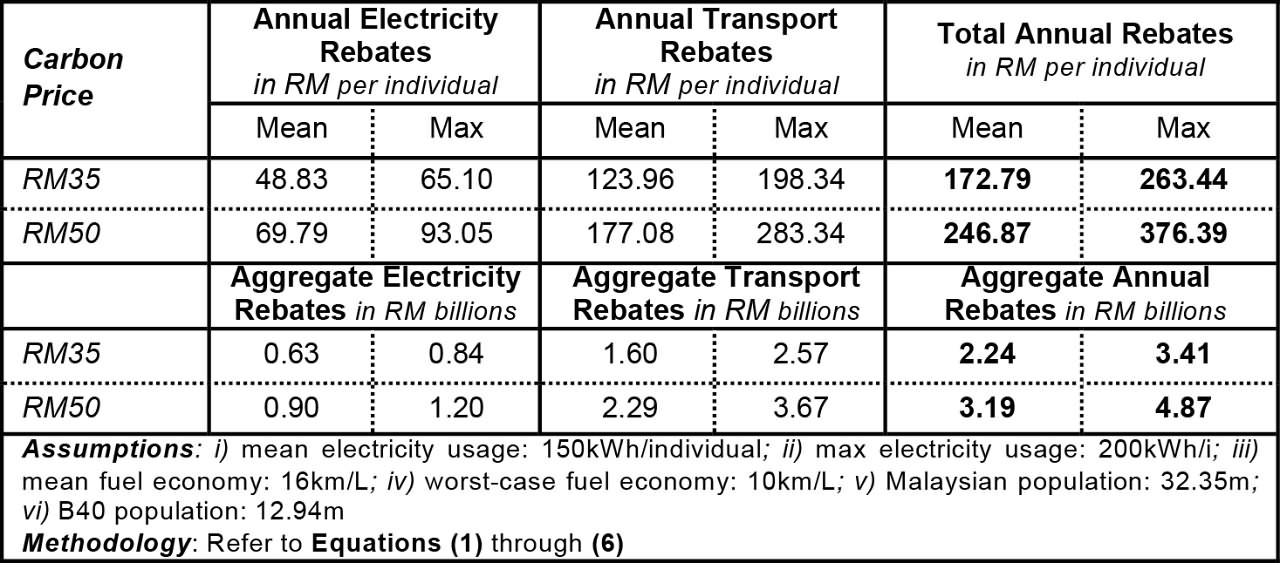

The worst-case carbon pricing-induced increases in monthly electricity and transport costs faced by consumers were noted earlier; Table 6 annualises those figures on both per individual and aggregate bases in order to quantify the total costs faced by consumers, and total rebate costs faced by the government, during each of the first four years of this policy.

Carbon rebates are an essential component of ensuring that carbon pricing aids, rather than hinders, the maximisation of social welfare. While Malaysians will face the same tax rate on carbon across income levels, rising electricity and transport costs will place a relatively heavier burden on lower-income households. These regressive effects would exacerbate an already-worsening picture of equality in Malaysia, but the utilisation of carbon revenues to compensate members of the B40, and possibly less-well-off members of the middle 40% (M40), would go a long way in mitigating this issue.

Table 6: Annual Carbon Rebates at RM35 and RM50/tCO2e

Individuals within the B40 are estimated to require rebates of between RM172 and RM264 per annum at a carbon price of RM35/tCO2e, and between RM246 and RM377 at RM50/tCO2e. To the government, this would come at a cost of between RM2.24 and RM3.41bil of federal carbon revenues at a price of RM35/tCO2e, and between RM3.19 and RM4.87bil at RM50/tCO2e[21]. This equates to a share of only 29.2–44.5% of carbon revenues across these four years[22].

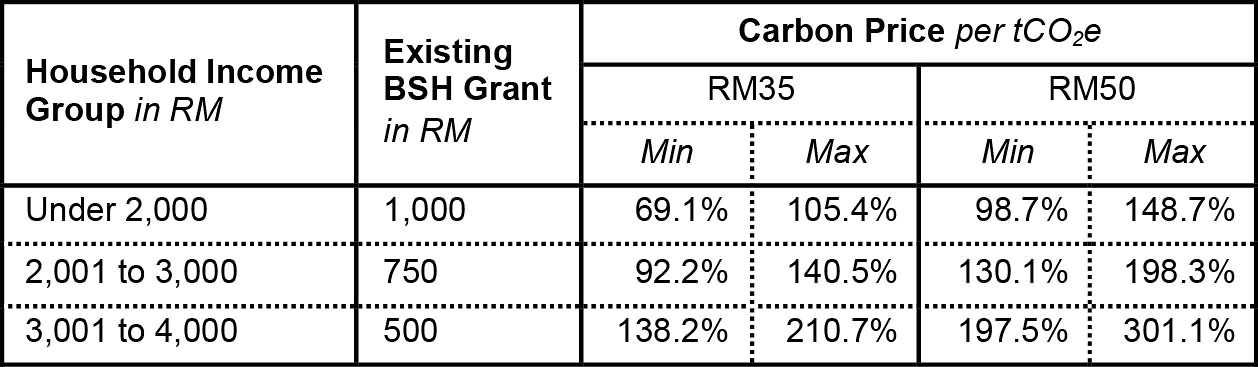

These carbon rebates should be dispersed alongside existing Bantuan Sara Hidup (BSH) payments, under which B40 households are already allocated fixed annual grants based on household income subgroup. Under the introductory carbon price of RM35/tCO2e, BSH grants inclusive of carbon rebates would rise by 69.1%–105.4% for households of four[23] earning under RM2,000 per month, for instance and, ceteris paribus, this figure increases to 98.7%–148.7% at the higher carbon price of RM50/tCO2e (see Table 7). Carbon rebates, in significantly increasing the size of annual grants afforded to the B40, can play a major role in improving the social wellbeing of Malaysia’s low-income households, who can profit even further by reducing their carbon footprints through investing in and using low-carbon technologies.

Table 7: Marginal Impact of Annual Carbon Rebates on Bantuan Sara Hidup Grants per household of 4

Furthering Climate Change Mitigation and Adaptation Efforts

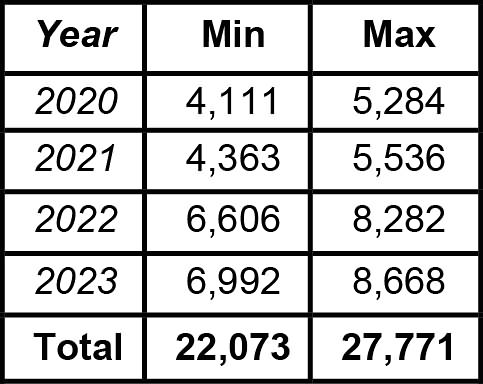

Table 8 provides a summary of residual carbon revenues from 2020 to 2023, assuming business as usual (BAU) emissions, after the regressive direct effects of the implementation of carbon taxation are addressed. It is estimated that in 2020, for instance, between RM4.11 and RM5.28bil will be available in funding for other initiatives of importance. By 2023, this figure is projected to rise to between RM6.99 and RM8.67bil, owing in part to projections of increasing emissions, but predominantly due to the change in the carbon price from RM35 to RM50/tCO2e.

Table 8: Residual Annual Carbon Revenues, 2020 to 2023 in RM mil, assuming BAU emissions

Malaysia being a nation with a significant need for continued decarbonisation, the ability to draw on additional financing streams for climate change mitigation measures, such as a greater penetration of RE, the adoption of energy efficiency measures, and forest

conservation efforts, is imperative. This need is quoted by MESTECC in its 2018 report to the United Nations Framework Convention on Climate Change, alongside the requirements of funding for adaptation measures and improved GHG inventory management systems; in fact, the taxing of carbon will place greater importance on the ability to reliably measure emissions, especially within policy-relevant sectors.

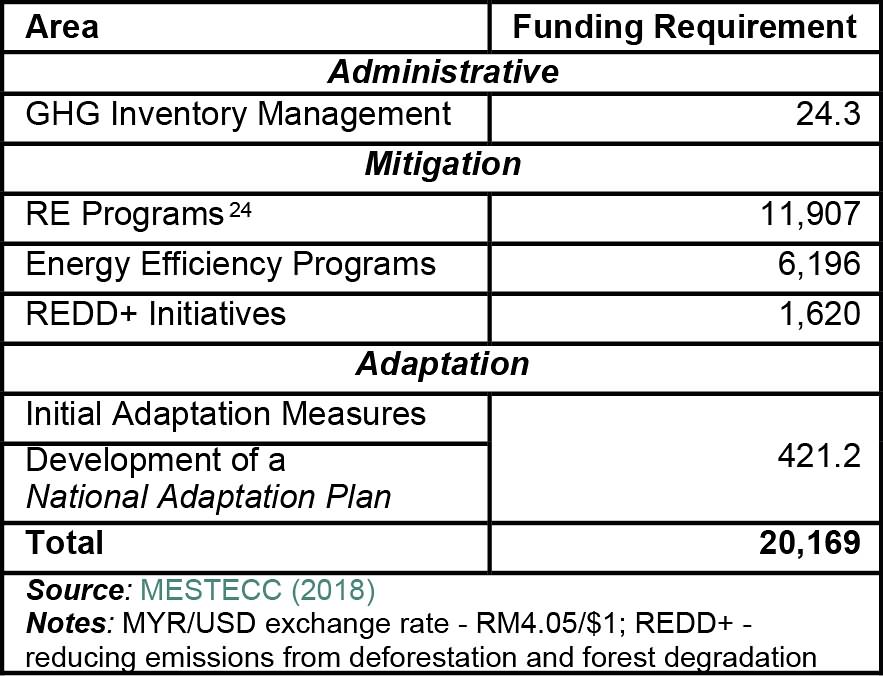

It is likely that more investment will be necessary to ensure the government’s ability to consistently monitor emissions and accurately enforce carbon taxes across firms in the electricity and oil and gas sectors most prominently. A full list of the climate change-related finance gaps cited by MESTECC is provided in Table 9. Crucially, these gaps can be met in their entirety within the first four years of the carbon pricing framework proposed in this paper, even at carbon rates as low as RM35 and RM50/tCO2e. This opportunity should be grasped.

Table 9: Malaysia’s Climate-Related Funding Gaps in RM mil

It will almost certainly be the case that sustained climate change mitigation and adaptation efforts continue to require ever-larger magnitudes of funding. Proceeds from carbon taxation should therefore be used to provide a stable, long-run source of financial support for these initiatives. Such significant investment in the domestic green economy will have strongly positive repercussions for the Malaysian economy at-large, adding momentum to the growth of a group of industries which are, and will continue to be, the centrepieces of sustainable development over the coming decades.

As was noted earlier, there are numerous other options the government should consider with regard to reducing the emissions intensity of, particularly, the transport sector, through an emphasis on public transportation and the use of energy-efficient vehicles. These endeavours would also require large sums of investment, and this illustrates succinctly the fact that MESTECC’s cited climate-funding needs are far from exhaustive. Malaysia’s ability to effectively manage and reduce emissions nationwide is heavily dependent on the ability of the government to raise the requisite funding for all important climate initiatives. In this regard, CPR can play an almost irreplaceable role.

Note

This document acts as policymakers’ summary of a more extensive paper published by the Penang Institute entitled Using Carbon Pricing to Support Sustainable Development in Malaysia. Please refer to that study for more detailed expression of the case for carbon pricing, and of this proposal in particular, as well as an exhaustive list of references and recommended reading.

Appendix

References

Azhgaliyeva, D; Kapsaplyamova, Z; & Low, L. 2018. “Implications of Fiscal and Financial Policies for Unlocking Green Finance and Green Investment”. ADBI Working Paper No. 861. Asian Development Bank Institute: Tokyo, JP. Available at www.adb.org/sites/default/files/publication/445076/adbi-wp861.pdf

Fabra, N & Reguant, M. 2014. “Pass-Through of Emissions Costs in Electricity Markets”. American Economic Review, American Economic Association: 104 (9), 2872-2899

Intergovernmental Panel on Climate Change. 2018. “Global warming of 1.5°C: An IPCC Special Report on the impacts of global warming of 1.5°C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty”. World Meteorological Organization: Geneva, Switzerland. Retrieved from www.ipcc.ch

International Renewable Energy Agency. 2018. “Renewable Power Generation Costs in 2017”. IRENA: Abu Dhabi, AE. Available at www.irena.org/publications/2018/Jan/Renewable-power-generation- costs-in-2017

Khazanah Research Institute. 2018. “The State of Households 2018: Different Realities”. Khazanah Research Institute: Kuala Lumpur, MY. Available at www.krinstitute.org/assets/contentMS/img/ template/editor/FullReport_KRI_SOH_2018.pdf

Malaysia. Ministry of Energy, Science, Technology, Environment and Climate Change. 2018. “Malaysia: Third National Communication and Second Biennial Update Report to the UNFCCC”. Retrieved from www.mestecc.gov.my

Malaysia. Ministry of Finance. 2018. “Fiscal Outlook and Federal Government Revenue Estimates 2019”. Retrieved from www1.treasury.gov.my/fo_2019.html

Malaysia. Suruhanjaya Tenaga. 2018. “Electricity Tariff Review in Peninsular Malaysia for Regulatory Period 2 under Incentive-based Regulation Mechanism”. Available at www.policy.asiapacificenergy. org/sites/default/files/Electricity%20Tariff%20Review%20in%20Peninsular%20Malaysia%20for%20R egulatory%20Period%202%20%28RP2-%202018-2020%29.pdf

Malaysian Institute of Road Safety Research. 2014. “Car Annual Vehicle Kilometer Travelled Estimated from Car Manufacturer Data – an Improved Method”. World Research and Innovation Convention on Engineering and Technology 2014: Putrajaya, MY.

Monnin, P. 2015. “The Impact of Interest Rates on Electricity Production Costs”. Discussion Notes

1503, Council on Economic Policies. Available at www.cepweb.org/wp-content/uploads/CEP_DN

_Interest_Rates_Energy_Prices.pdf

Ondraczek, J; Komendantova, N; & Patt, A. 2015. “WACC the Dog: The Effect of Financing Costs on the Levelized Cost of Solar PV Power”. Renewable Energy, 75 (3): 888-898

Petronas. 2018. “Moving Forward Together: Sustainability Report 2017”. Available at www.petronas.com/ws/sites/default/files/2018-07/sustainability-report-2017.pdf

Ricke, K; Drouet, L; Caldeira, K; & Tavoni, M. 2018. “Country-Level Social Cost of Carbon”. Nature Climate Change, 8 (10): 895-900

United States. Energy Information Administration. “Annual Energy Outlook 2019 with Projections to 2050”. EIA at the United States Department of Energy: Washington, D.C., USA. Available at www.eia.gov/outlooks/aeo/pdf/aeo2019.pdf

United States. Interagency Working Group on Social Cost of Carbon. 2016. “Technical Support Document: Technical Update of the Social Cost of Carbon for Regulatory Impact Analysis Under Executive Order 12866”. Available at www.epa.gov/sites/production/files/2016-12/documents/sc_co2_tsd_august_2016.pdf

United States. Interagency Working Group on Social Cost of Carbon. 2010. “Technical Support Document: Social Cost of Carbon for Regulatory Impact Analysis Under Executive Order 12866”. Available at www.epa.gov/sites/production/files/2016-12/documents/ scc_tsd_2010.pdf

World Bank. 2017. “Report of the High-Level Commission on Carbon Prices”. High-Level Commission on Carbon Prices, Carbon Pricing Leadership Coalition. World Bank: Washington, D.C., USA. Available at https://www.carbonpricingleadership.org/report-of-the- highlevel-commission-on-carbon-prices

World Bank & Ecofys. 2018. “States and Trends of Carbon Pricing 2018”. World Bank: Washington, D.C., USA. Available at https://openknowledge.worldbank.org/bitstream/handle/10986/29687/9781464812927.pdf

Zaid, S & Graham, P. 2017. “Rising Residential Energy Consumption and GHG Emissions in Malaysia: A Case Study of Public Low-Cost Housing Projects in Kuala Lumpur”. Indoor and Built Environment, 26 (3): 375-391

[1] For a good to be non-rivalrous, any one individual’s access to a particular resource, in this case the atmosphere, should not have an effect on another individual’s ability to access to the same resource. Non-excludability refers to the notion that no individual can be restricted from using the resource in question.

[2] Alberta: the SCC rises from C$20 in 2017 to C$30/tCO2e in 2018; British Columbia: annual rise of C$5 annually and peaking at C$50 in 2021; France: annual rise of €10.40 and peaking at €86.20 in 2022; Netherlands: floor price on carbon will rise from €18 in 2020 to €43 in 2030; Singapore: S$5 until 2023 and rising to $10–15 thereafter. See World Bank (2018) for more details on existing and planned carbon pricing policies globally.

[3] In total, 99.86% of fugitive methane emissions arise from oil and natural gas production, with the remaining 0.14% from solid fuel sources. Natural gas alone is responsible for 96.56% of total fugitive methane emissions (MESTECC, 2018).

[4] Or downstream carbon pricing regulation.

[5] Emphasis is placed on these energy inputs as they have thus far in 2019 accounted for a combined share of 96.5% of Malaysia’s electricity mix.

[6] The first of these is RM14.47/MMBtu, reflective of the official coal price under Regulatory Period 2 (RP2) of the Incentive-Based Regulation (IBR) mechanism (Suruhanjaya Tenaga, 2018). The second figure, of RM16.59/MMBtu, assumes a growth rate in the price of coal equivalent to that between RP1 (RM12.43/MMBtu) and RP2.

[7] The average global per unit costs of utility-scale solar power generation in 2017 were almost three-quarters lower than in 2010, falling from US$0.36/kWh to $0.10/kWh, and are projected to reach as low as $0.065/kWh (RM0.26/kWh) by 2020. See IRENA (2018) and EIA (2019) for more detailed information on the costs of electricity generation from renewable sources between 2010 and 2050.

[8] See Azhgaliyeva et al (2018); Ondraczek et al (2015); and Monnin (2015).

[9] In fact, financing costs are found to have a more significant impact on the LCOE of solar than local levels of solar irradiation.

[10] The economic literature investigating cost pass-through in electricity markets where emissions are priced indicates pass-through rates of 77–86% (Fabra and Reguant, 2014).

[11] These figures are reflective of those reported by Single Buyer (www.singlebuyer.com.my), the entity charged by the Minister of Energy to manage electricity planning and procurement services within Peninsular Malaysia. In determining the breakdown of natural gas contributions through the twin channels of open- and combined-cycle plants, it is assumed that roughly 14% of natural gas power generation is delivered by OCGTs. This equates to the share of OCGTs in Peninsular Malaysia’s total natural gas power generation capacity.

[12] Zaid and Graham (2017), in perhaps the most comprehensive analysis of residential energy consumption in Malaysia, study two low-cost housing projects in Kuala Lumpur, and find per-occupant usage to be between 78 and 140kWh per month. This result is here used to estimate the impact of carbon pricing on the wellbeing of the nation’s B40, particularly if, as is theorised, variations in electricity consumption are explained to a significant degree by income.

[13] Assuming the remaining 80% of electricity generation in 2025 is comprised of coal (30%), and CCGT (50%).

[14] This calculation assumes an annual average of 24,129.1km driven per vehicle (Malaysian Institute of Road Safety Research, 2014).

[15] MESTECC (2018) reports that just under 88% of transport-sector emissions arise from road transportation. Within this subgroup, private vehicles are biggest polluters.

[16] Given that public transport is strictly less emissions-intensive than any private alternatives, any action that induces a shift in demand from the latter to the former would lead to a reduction in aggregate sub-sectoral emissions.

[17] High-income earners are more found to be more unresponsive to changes in fuel costs, and this highlights the importance of strong policy measures which succeed in improving fleet-wide fuel economy.

[18] This should be at least until such a point where the electricity grid is clean enough that even a sizable fleet of EVs would minimise emissions within the sector.

[19] Under BAU emissions, average annual revenues between 2020 and 2030 are estimated at RM24.57bn, with total revenues over the period amounting to RM270.28bn; and under PLAN and AMB emissions, these are RM23.39bn and RM257.69bn, and RM21.8bn and RM239.78bn, respectively.

[20] An important caveat is that two factors may adversely affect actual carbon revenue collections. The first of these are the possibility that economic actors subjected to carbon pricing may understate emissions; this heightens the importance of ensuring a robust and comprehensive ability to monitor emissions within the relevant sectors. Second, any success this carbon pricing policy has in shifting actual emissions to levels even below those projected under MESTECC’s AMB plan would also contribute to lower revenue collections. This, however, would be a positive development from the perspective of climate action.

[21] If steps were taken to mitigate the regressive effects of carbon taxation on the middle 40% (M40) as well, at a rate half that of the B40, aggregate compensation costs would rise by roughly 150% –still enough to ensure leftover funding for other important policy initiatives. Given the rather limited absolute magnitude of the effects on electricity and transport costs, such a move may not even be entirely necessary – if anything, it may be pragmatic to extend some remuneration to only a subset of the M40.

[22] Generally speaking, the proportion of revenues which need to be utilised to compensate the B40 decreases as the price of carbon rises. This, ultimately, leaves more excess revenue over time through which the government can address other funding needs it may have.

[23] Khazanah Research Institute (2018) reports the average household size as approximately 4.1 people.

Managing Editor: Ooi Kee Beng, Editorial Team: Regina Hoo, Braema Mathi, Alexander Fernandez and Nur Fitriah (designer)

You might also like:

![[Rapporteur Notes] Penang Economic Summit 2022: The Post-Pandemic Economic Reset]()

[Rapporteur Notes] Penang Economic Summit 2022: The Post-Pandemic Economic Reset

![Policymaking and Implementation: Shifting from Hierarchies to Interdependent Polycentric Networks]()

Policymaking and Implementation: Shifting from Hierarchies to Interdependent Polycentric Networks

![A Critical Time for Penang's Fragile Creative Ecosystem]()

A Critical Time for Penang's Fragile Creative Ecosystem

![The Future of Creative Industries in Penang]()

The Future of Creative Industries in Penang

![Survey on Attitudes to Covid-19 Vaccination in Penang]()

Survey on Attitudes to Covid-19 Vaccination in Penang

![[Rapporteur Notes] Penang Economic Summit 2022: The Post-Pandemic Economic Reset](https://penanginstitute.org/wp-content/uploads/2022/12/thumbnail-1-150x150.jpg)